Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

IN THIS PAPER

The rise of the real asset portfolio. The concept of the “real asset,” “tangible asset” or “inflation-sensitive” portfolio, firmly established in certain asset owner circles, has gained ground in recent years. While the post-GFC phase was marked by diversification toward real assets, later years have seen greater emphasis on diversification within real assets, towards sectors such as agriculture.

Diversification under scrutiny. The new mindset prioritises characteristics or risk factors rather than labels. Yet, as is becoming increasingly clear late in the cycle, these characteristics are not hard-wired to real assets. Current conditions have produced greater tensions between particular traits, such as ‘yield’ and ‘low correlation to equities.’

Implementation questions. Many investors are building out diversified real asset exposures directly. Managers are changing the way they deliver these strategies, including taking advantage of their new organisational breadth across this space. The paper explores a relatively new approach that is increasingly widely available: multi-real-asset.

WHY DOWNLOAD?

As investors have moved towards “real asset” portfolios rather than segregated sector-specific buckets, three significant trends have emerged.

The heart of this often-discussed shift is a mindset that is less focused on labels and prioritises core characteristics or risk factors, such as inflation sensitivity, diversification from equity and yield. Yet, as is becoming increasingly clear late in the cycle, these characteristics should be handled with care.

The first trend: while unlisted real estate and infrastructure often sit at the heart of real asset portfolios, investors are becoming increasingly sophisticated and granular in their approaches. Secondly, holistic approaches have facilitated diversification into niche sectors that may not sit within the old buckets, such as agriculture.

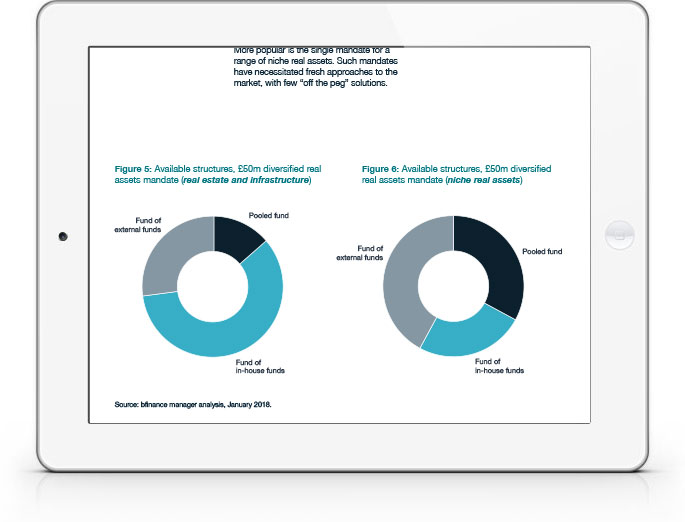

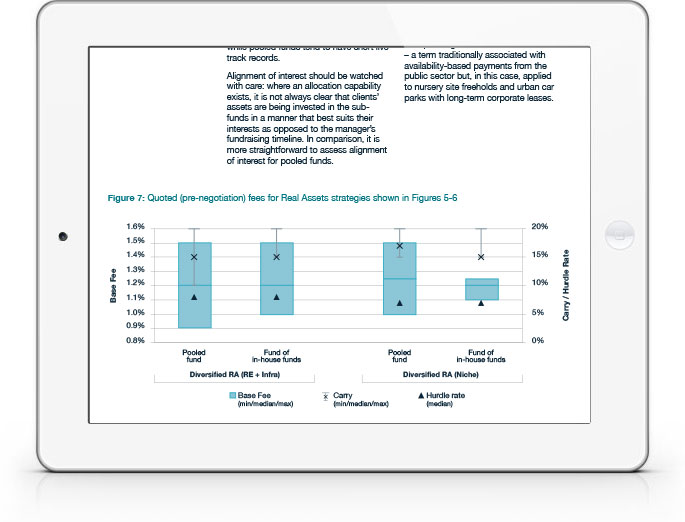

The third and newest development is the rise of multi-real-asset investment strategies. Asset managers are launching strategies or structuring wrappers that offer breadth across multiple sectors. Structures range from “funds of in-house funds” to true diversified pooled funds. In some ways this latest step was a logical extension to major shifts in the asset management industry, where many firms have now built or branded broad real asset divisions.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.