Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

IN THIS PAPER

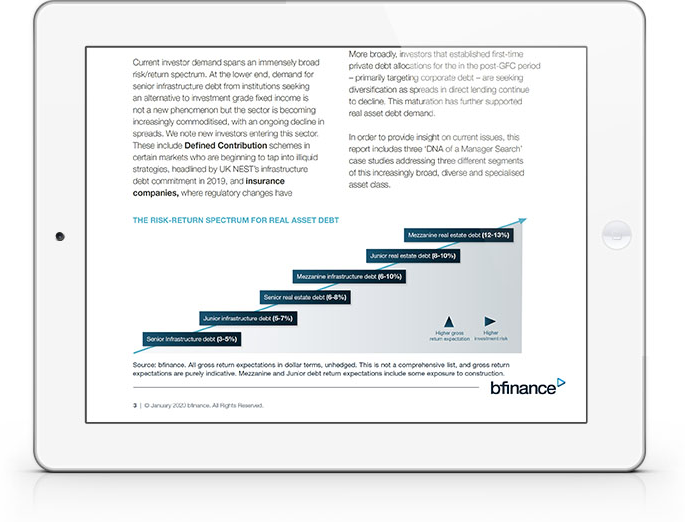

Understanding the “real asset debt” risk-return spectrum, ranging from very low risk senior infrastructure debt strategies to mezzanine real estate debt funds targeting gross returns of >12%. Recent years have seen spread compression, more product commoditisation at the “safer” end, and the emergence of new options such as infrastructure direct-lending type strategies.

Comparing global opportunities. With investors increasingly looking beyond their back yard, the report highlights key geographical differences including current return expectations, typical loan types, fund structures, leverage, degree of institutionalisation, fees and more.

The importance of customisation. Case studies emphasise highly specific needs of particular clients, who are entering real asset debt for very different purposes ranging from safe fixed income alternative to real estate replacement. ESG and gender diversity requirements, tailored separate account structures, deal size constraints, the need for floating versus fixed-rate debt and much more.

WHY DOWNLOAD?

At bfinance, 2019 brought the first ever year in which searches conducted by investors for “Real Asset Debt” outweighed, in dollar terms, searches for corporate Private Debt. Recent appetite for real asset debt, and particularly infrastructure debt, is also reflected in global fundraising statistics.

We note new investors entering this sector. These include Defined Contribution schemes in certain markets who are beginning to tap into illiquid strategies, headlined by UK NEST’s infrastructure debt commitment in 2019, and insurance companies, where regulatory changes have improved treatment for unrated debt in general and infrastructure debt in particular. More broadly, investors that established first-time private debt allocations for the in the post-GFC period – primarily targeting corporate debt – are seeking diversification as spreads in direct lending continue to decline. This maturation has further supported real asset debt demand.

Current investor appetite spans an immensely broad risk/return spectrum. At the lower end, demand for senior infrastructure debt from institutions seeking an alternative to investment grade fixed income is not a new phenomenon but the sector is becoming increasingly commoditised, with an ongoing decline in spreads. At the riskier end we are seeing pension funds with real estate and infrastructure equity portfolios shifting towards debt.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.