Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Niels Bodenheim

Senior Director, Private Markets

Unitranche debt / loans, which increasingly dominate European private debt funds and also play a key role in the US market, were only invented a decade ago. GE and Allied Capital (later Ares) teamed up to offer a single-tranche of lending where the first-out position was provided by GE and the second-out by Allied. The borrower received one set of pricing and one loan agreement: for them it was more expensive but simpler and, importantly, enabled greater leverage.

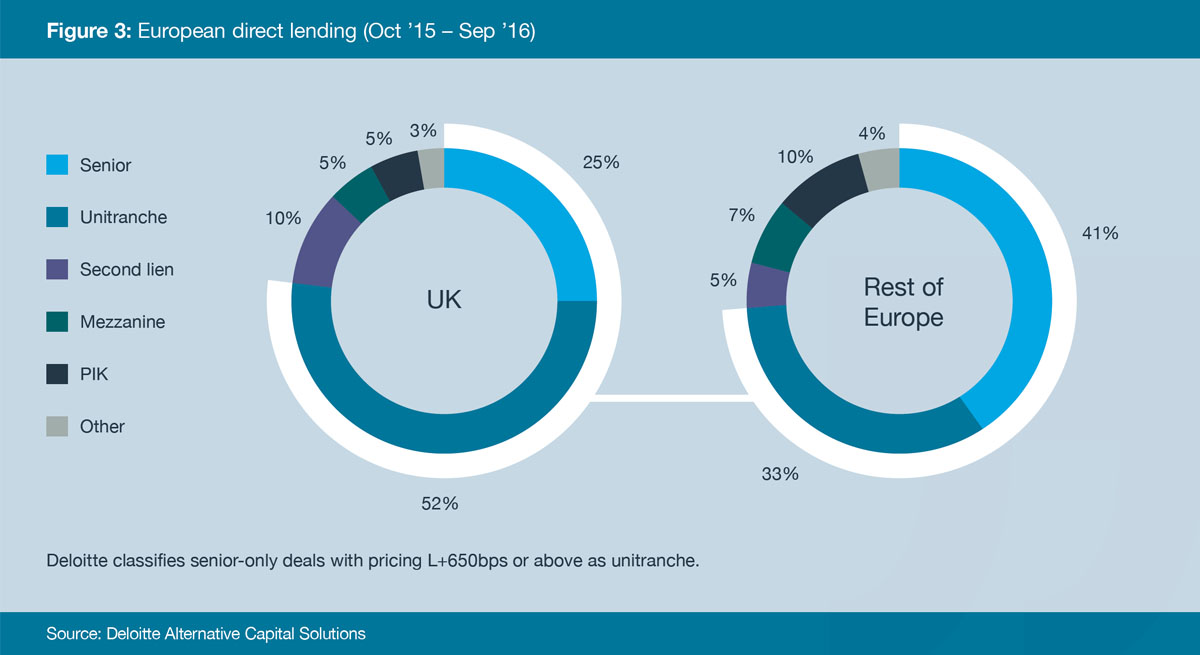

Within ten years, unitranche has gone from novel concept to instrument of choice (Figure 3). For managers, the unitranche has provided a way of boosting returns without adding further to the proportion of subordinated debt in portfolios, since it is technically first-lien. For many banks, unitranche has been the source of new lending partnerships with asset managers.

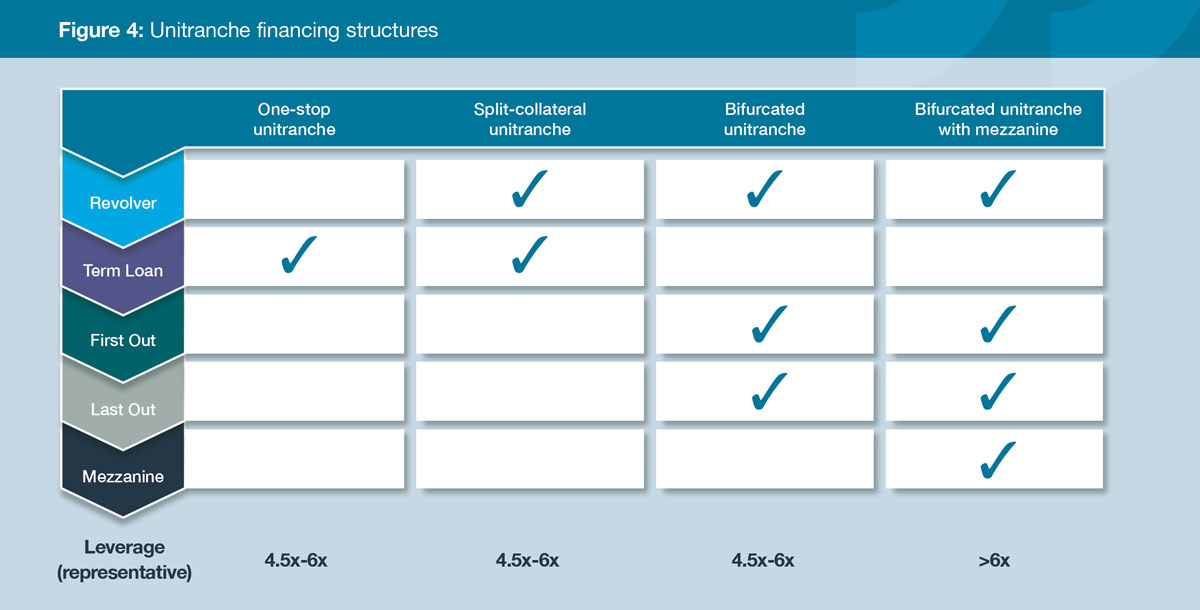

Investors, however, should keep a careful eye on the structures and terms underpinning these loans. While more than 80% of the unitranche debt in the senior portfolios we’ve analysed during the past six months represents a simple term-loan or term-loan-plus revolver structure, a range of increasingly complex models have emerged, effectively replicating a variety of conventional financing options such as incorporating second-lien or even mezzanine. These are shared among multiple parties via an Agreement Among Lenders (AAL) - formerly simple five-page documents, now frequently far longer.

We’re seeing lenders introducing a component of PIK (Payment in Kind) relative to cashpay in unitranche, enhancing returns but creating a more back-ended structure (deeper J-curve). This increases duration risk on what are usually 7- or 8-year loans in Europe and 5- or 6- years in the US. We’re also seeing more cases where the unitranche is going deeper into the capital stack, which can be a source of concern for a loan classified as senior debt. Cash flow debt multiples are now at the upper end of historical levels, with figures of 6x or higher deserving particular scrutiny.

If there is a significant revolver (revolving credit facility) being provided by a party other than the manager then that provider, usually a bank, should be seen to represent the true first-out (or super-senior) position. More broadly, those holding first-out positions within unitranche deals are not necessarily treated as advantageously as traditional first-lien lenders in the event of default and workout. It is additionally unclear that all AALs would carry the same force in courts as standard intercreditor agreements, although signs have so far been positive.

Most importantly, although we have seen some restructuring of unitranche deals, we have not yet seen how they fare through a full credit cycle. That being said, today’s higher purchase price multiples (and lower Loan-to-Value ratios) do build in a higher proportion of equity in deals, providing something of a safety net for lenders.

This article is an extract from the March 2017 bfinance white paper Direct Lending: What’s Different Now? Readers can download a free copy of the report, which includes analysis of recent shifts in the private debt market and detailed insights from recent bfinance manager searches.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.