Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Toby Goodworth

Managing Director, Head of Risk & Diversifying Strategies

After a troubled 2018, 2019 proved to be a far better year for hedge funds and alternative risk premia. Yet the “diversification” question remains top-of-mind – and problematic.

As of end-October the HFRX Global Hedge Fund Index up 6.2% to end-October and the HFM Global Index up 5.6%. [See Manager Intelligence and Market Trends for full-2019 performance data.] This period has generally rewarded equity risk exposure, with more volatile – and often more directional or market-exposed – strategies posting higher returns. For example, the HFM Global Equity Index, with a five-year beta of 0.38 to global equities, was up +8.7% in the first ten months of 2019, making it the highest-performing subset of the hedge fund universe. The HFRI Equity Market Neutral index, conversely, was up just 2%. EMN strategies have missed out on the uplift provided by rising equity markets, and have also suffered from the continued underperformance of fundamental equity value factors.

If hedge funds were train operators, Q4 2018 featured the wrong type of leaves on the line.

THE D WORD

Yet the strong results for equity-focused hedge funds in 2019 are not reflected in investor appetite among bfinance’s client base of pension funds and other asset owners. We have seen very little demand for hedge funds with moderate equity risk exposure, or indeed for strategies focusing on a single asset class. We have also seen very weak demand for very defensive relative value / arbitrage type strategies, despite strong performance (+5.8% to end-Oct).

Instead, robust diversification has been the central objective for many institutional clients within their liquid alternative portfolios. This has typically meant multi-asset, multi-style strategies. The majority of liquid alternative searches from bfinance clients in 2019 have involved taking exposure from equity risk and channelling it towards non-equity risk, while maintaining a reasonable rate of return. This has led to continued emphasis on segments such as Multi-strategy Absolute Return, Macro, CTAs, and Alternative Risk Premia.

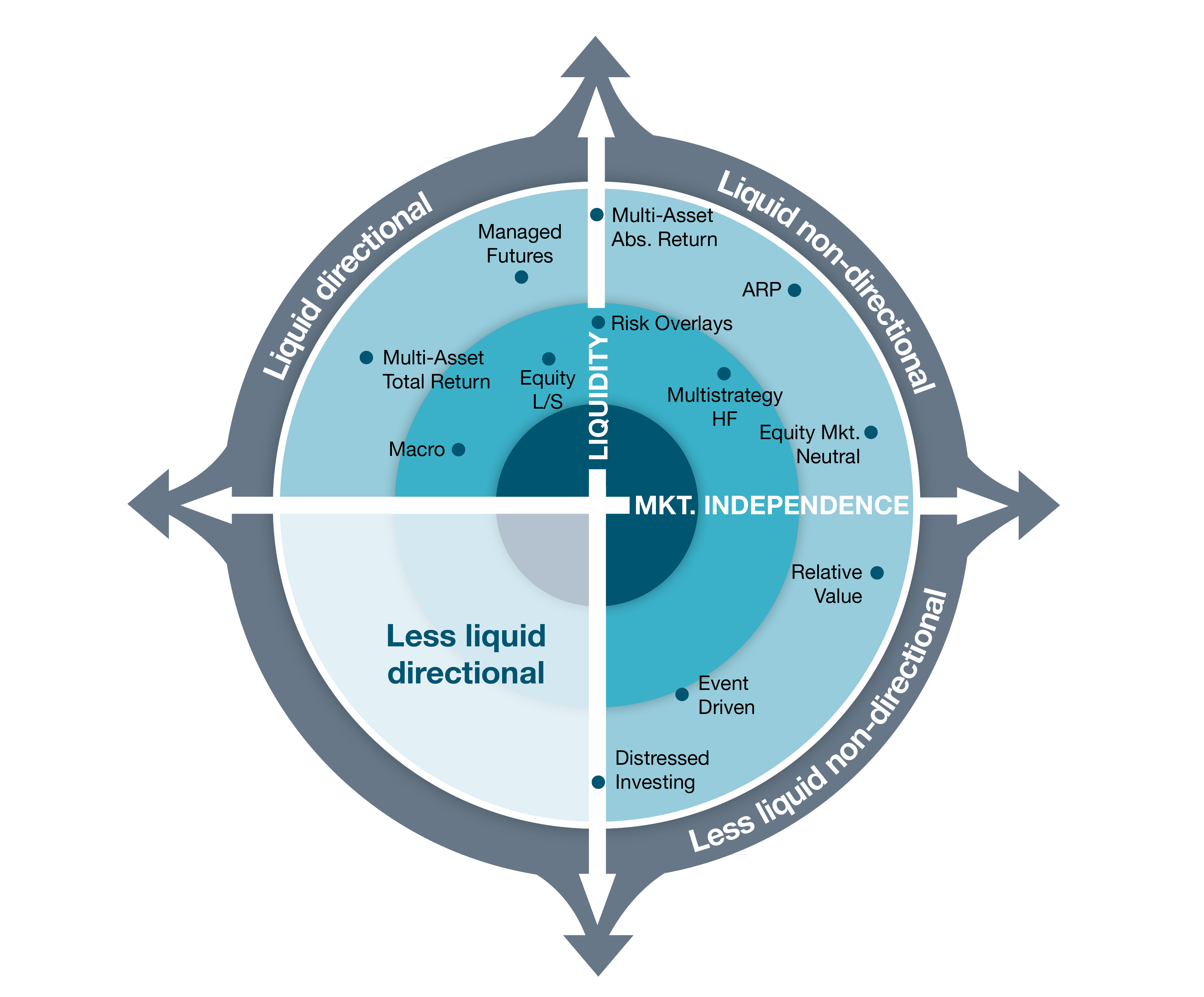

ALTERNATIVE INVESTMENT STRATEGIES, BY LIQUIDITY [OF VEHICLE] AND EQUITY MARKET DIRECTIONALITY

Source: Five Levers for Reducing Equity Risk

These sectors have also produced some of the year’s better performers. Global Macro strategies are up on average 5.5% to end-October, with Systematic Macro strategies generally outperforming their Discretionary counterparts, although individual manager dispersion within this space remains significant. Meanwhile Managed Futures strategies are up 6%, down from around +12% at end-August: returns in this space have been driven almost exclusively by fixed income trends, both on the upside and more recently to the downside. This year therefore potentially breaks an extended weaker run of average performance for CTAs, which broadly lost money in 2018 and delivered flat-to-negative returns from 2015 to 2017. Even then, the weak returns did not put investors off by any means. Global Macro and CTAs represent some of the few strategies that potentially offer investors meaningfully convex returns – outsized positive performance when markets are stressed and falling. Greater uncertainty, and increased dispersion in global growth and central bank activity, should provide a strong opportunity set for these managers.

Another source of potentially convex returns; Volatility Arbitrage, has had a relatively muted 2019 - up just +3.8% to end-October against a background of still-compressed volatility levels. Event Driven strategies have also fared positively in 2019, typically up over 5% to end-October after a poor 2018. Within this sector, the more market-independent Merger Arbitrage strategies have continued their long run of positive performance, with average returns above 4%. M&A activity for 2019 currently looks to be down on last couple of years in terms of deal numbers and volumes, according to Bloomberg data, but average premium levels have remained attractive.

ALTERNATIVE RISK PREMIA STRATEGIES RETURN TO FORM

Meanwhile, we have observed a resurgence in appetite among our clients for Alternative Risk Premia. This group of strategies experienced their first year of negative average returns in 2018 – a result that certainly led many investors to pause for thought in early 2019. Yet their performance appears to be ‘back on track,’ with the bfinance ARP composite up over 4% to end-October, largely neutralising the losses of 2018 (-5%). The high dispersion of manager returns in ARP continues to illustrate the wide range of implementation approaches, including the choice of which premia to use and how they are combined. 2019 has seen a continued blurring of boundaries between ARP and hedge funds, with more complex variants proving increasingly difficult to distinguish from systematic macro.

In some ways, Alternative Risk Premia continues to tap into the zeitgeist in terms of institutional client demand, offering liquidity, low net equity exposure and relatively low cost. We are also seeing hedge fund clients continuing to lean towards systematic versus discretionary strategies, partly due to costs but also due to the persistence of style exposures. All these points favour continued support for the ARP sector.

IS DIVERSIFICATION REALLY WORKING

Despite the overarching emphasis on diversification, the ‘D-word’ remains something of a conundrum. With equity performance continuing to be positive, diversification has not really had a chance to prove its colours during recent years. Indeed, during the limited periods when equity markets have done badly – such as the final quarta horribilis of 2018 – plenty of diversifying strategies failed to cover themselves in glory. If hedge funds were train operators, that quarter featured ‘the wrong type of leaves on the line.’ Ultimately, an explicit diversifying exposure that fails to provide diversification at exactly the point when it matters most must surely be open to some uncomfortable questions.

When it comes to diversification, hedge funds and liquid alternatives must also compete for attention versus the still-growing unlisted investment sectors such as private equity, private debt and infrastructure. It is a competition that ‘private markets’ have undoubtedly been winning recently in terms of manager search statistics. Yet a considerable proportion of the diversification offered by unlisted strategies lies in accounting optics – infrequent valuations, lack of visible volatility, lagged mark-downs.

When the markets do experience their next prolonged downturn, a clearer picture will emerge. We may witness a fundamental change in investors’ diversification agendas – and, by extension, the fundraising statistics.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.