Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Peter Hobbs

Managing Director, Head of Private Markets

For many years, real estate investment has retained a chronic home bias. Today, international diversification is on the rise. So why are there still so few “global” real estate funds, and what are the options for investors seeking global exposure.

The real estate asset class is over 50 years old. For much of this time, most of the capital involved has been deployed in domestic markets. For investors that have ventured overseas, the timing has frequently been terrible – British in the early 1970s, Japanese and Swedish in the late 1980s, Americans and Australians around 2007. At these times, investments were made at the top of the market, often with fickle partners.

The losses that followed seemed to reinforce the appeal of a home bias. Through these cycles, however, there has been a steady growth in ‘global’ investing, and key lessons have been learnt by investors and managers. Today, the options are more diverse, deep-rooted and better understood.

Does the current surge in international diversification signal a repeat of history?

Moving abroad

In the first half of 2018, bfinance has helped a number of investors in a range of searches that covered virtually the full spectrum of real estate investment: Core, Core+, Value Added and Opportunistic; Global and Regional; Unlisted and Listed (REITs); Equity and Debt; ‘Impact’ Real Estate. Yet there has been a common theme to the different projects during this period: each one has had an ‘international’ remit, with most of the investors seeking to deploy capital outside of their domestic markets.

Greater appetite for international real estate often tends to come at late stages of market cycles, when domestic real estate seems expensive and allocators are more motivated to look overseas. As noted above, these experiences have often ended unhappily, with wounded investors pulling back from international exposure. Does the current surge signal a repeat of history?

We would sincerely hope not, although the risks of real estate strategies are evidently elevated at such points in time. Firstly, today’s strong demand for international real estate is underpinned by a better appreciation of diversification characteristics. Unlike public equity and fixed income markets, which tend to be highly correlated across regions, there are significant differences across real estate markets, such that global exposure produces risk-reduction benefits. Secondly, the industry does seem to have learned from many of the mistakes from the past. There is a deeper awareness of the risks, accompanied by improvements in market transparency, better regulatory oversight and lower levels of leverage.

GLOBAL APPETITE ≠ GLOBAL FUNDS

In the face of this increased investor appetite for ‘global’ real estate investment, one might expect that there would be substantial growth of ‘global real estate fund’ offerings. Interestingly, this is not the case. Their numbers have increased modestly in recent years, primarily through the morphing of the fund of fund model whereby some fund of fund managers have begun taking direct positions in assets, often working closely with a group of operating partners. Yet, on the whole, there remain relatively few ‘global’ offerings at either the Value Add/Opportunistic or the Core/Core+ end of the spectrum.

The shortage of global unlisted real estate funds may be even more surprising when one considers three other significant trends. The first is the greatly increased size of large real estate managers and funds: the AuM of the top 20 real estate mangers has nearly trebled in the last fifteen years, now sitting around $1.5 trillion. The second is that investors are trending towards fewer/larger manager relationships rather than a larger number of small allocations. A smaller manager roster can mean lower monitoring costs, reduced governance risks and lower fees. Large mandates are a hallmark of today’s market: certain real estate houses won’t now offer a segregated mandate below the $500 million mark. The third trend is the surge of global REIT funds. Although individual REITs continue to have a mostly national or regional focus, there has been a significant growth in number of managers and funds that have a broad international remit, with bfinance estimating that over half of the largest 170 REIT fund offerings now have a global focus.

Each of these dynamics should, in theory, support the emergence of unlisted real estate funds (not just fund-of-funds) with a more global remit. These themes were explored in the recent bfinance insight paper: Rethinking Real Assets.

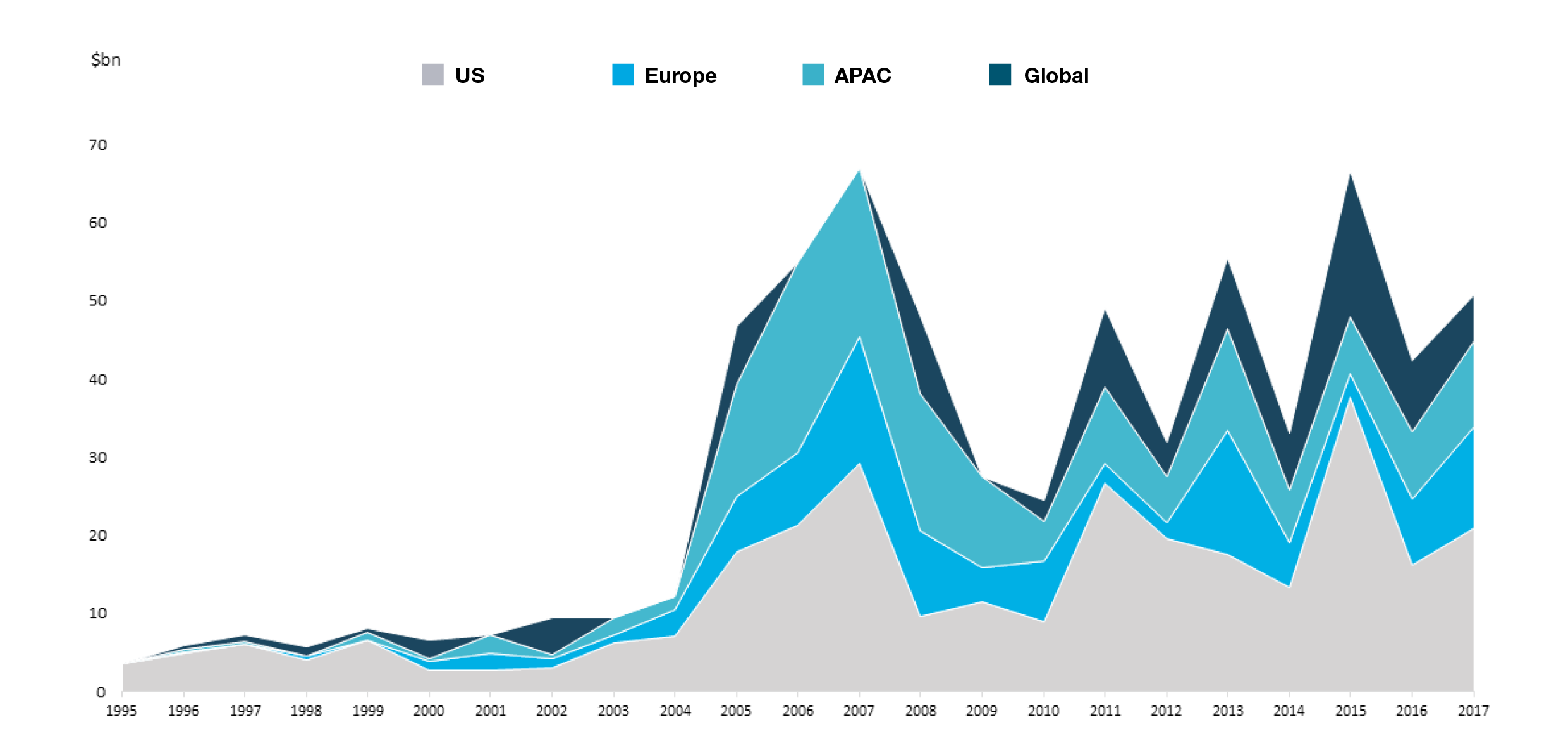

OPPORTUNISTIC STILL STUTTERING POST-GFC

Perhaps the strongest driving force for global real estate investing over the past 30 years has come from ‘Opportunistic’ funds. These originated in the aftermath of the S&L crisis of the early 1990s in the US. As distressed opportunities dried up in the US, these managers moved abroad to exploit similar opportunities, first in Europe and then in Asia.

The early vintages of these funds tended to be relatively successful and led to the steady growth in number and size of fund launches in the years up to the GFC. That being said, few of these were genuinely global strategies. There was a spike in capital raising in the GFC vintage (2005-2007), including a number of ‘mega funds.’

The Opportunistic asset class suffered catastrophically through the crisis and has only gradually gained back ground since then. Yet, despite the recovery, the focus has remained on regional rather than ‘global’ strategies.

Note: Based on capital raised in each vintage by primary focus of fund strategy

Source: bfinance; Preqin

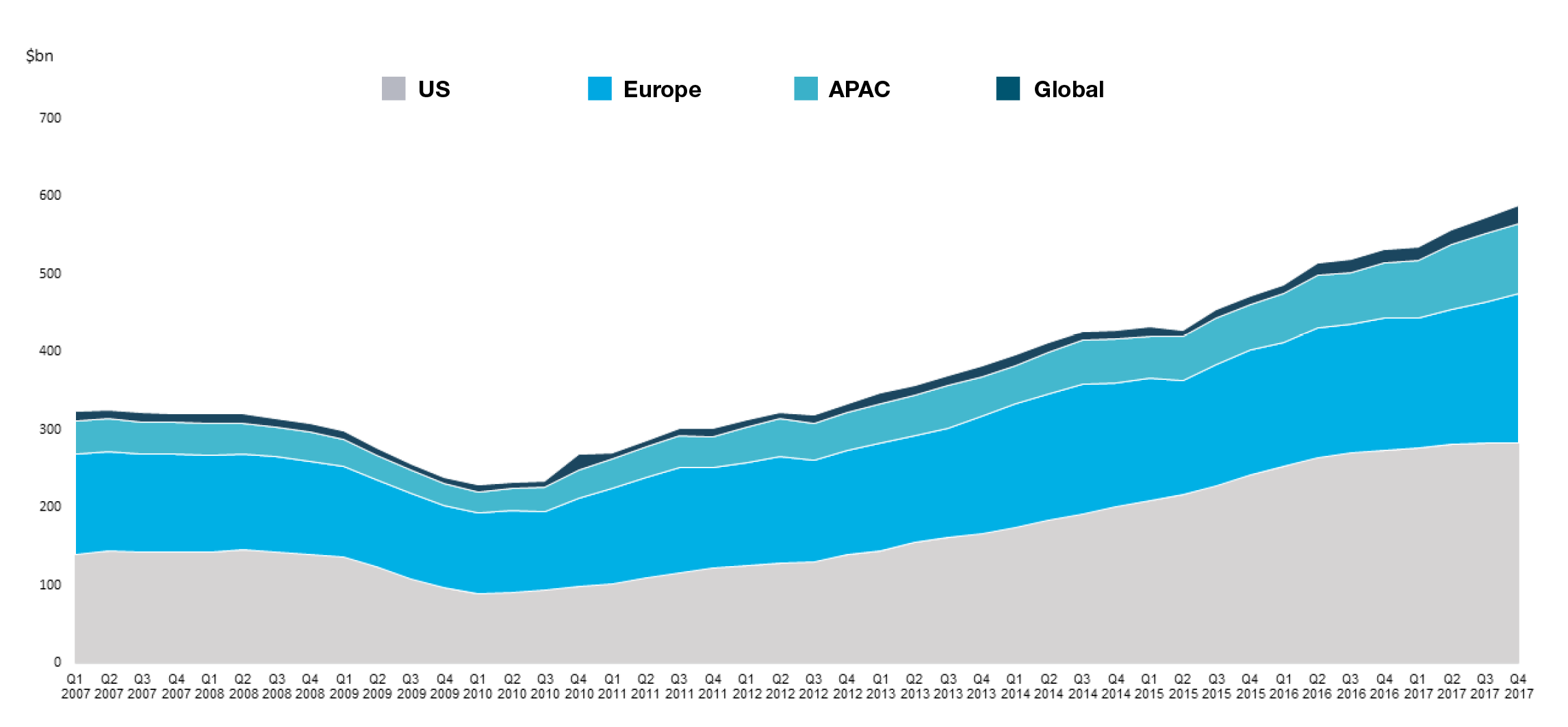

STRIKING SHORTAGE OF GLOBAL CORE FUNDS

With very few exceptions, there has been a limited tradition of managing Global Core strategies. The main exceptions have been German Open-End funds that have been investing internationally for many years. These ‘retail’ funds suffered from the requirement to provide high liquidity during the GFC, and have failed to regain their scale of their golden years, although there are a handful of these funds that have close to $15bn deployed in ‘global’ strategies. In addition, these funds are very geared towards German investors in terms of their valuation practices and governance. Beyond these, and despite the growth of Regional Core funds, there are few global Core or Core+ vehicles.

Source: bfinance, INREV, NCREIF. Based on estimated value of commingled open-ended funds in relevant regions.

Over the coming years, we believe that there will be an increase in the availability of structures providing 'global Core' exposure.

BUILDING AN INTERATIONAL PORTFOLIO

Beyond the potential use of REITs, investors have several options for building their exposure to global real estate. Each brings its own strengths and limitations:

1) Combination of funds. Multiple mandates spanning different regions and strategies remain the norm. Yet there is an interesting new dynamic in play: with the recent growth of global asset manager platforms, there is an increasing number of managers with capabilities – albeit separate – across the three main regions. This creates the opportunity for investors to access these regional funds from the same manager, with centralised reporting and oversight. There is strong momentum behind this approach in the Core space with many of the managers of US Core funds (the NCREIF ODCE funds) creating similar products in Europe and, more recently, in Asia Pacific. It is easier to combine exposure to these products as they are open-ended/evergreen while the closed ended Opportunistic funds are unlikely to be in the market at the same time in each region. Despite this, there are also instances of managers combining regional Value Added or Opportunistic offerings to provide global exposure for investors. The main challenge for investors seeking such strategies is to determine that each of the underlying funds is a suitable choice on a standalone basis versus local competitors.

2) Separate accounts with a global remit. These have the advantage of being tailored to the needs of the specific investor. The major downsides relate to their scale (with most managers not willing to consider such mandates for less than $100m) and limited scope for diversification: even a $100m exposure would be unlikely to provide exposure to ‘global’ real estate and would likely be highly concentrated in a small number of assets.

3) Global funds. Whether direct or fund-of-funds, there is a modest number of global funds available outside of the German domiciled funds. These include some global ‘direct’ funds that are building portfolios of assets across international markets. They also include a number of former Fund of Fund managers who have come to take more direct control of assets and operating partner relationships. So there is an increasing spectrum of options, from traditional fund of funds through managers of operating partners to portfolios of directly held assets. Each of these options has its strengths and weaknesses. For instance, the fund of fund routes tend to be associated with higher total expense ratios due to the double layer of fees while they have the advantage of greater diversification by geography and assets than more directly held properties. The availability of these options is increasing, across the Core, Core+, Value Add and Opportunistic spectrum.

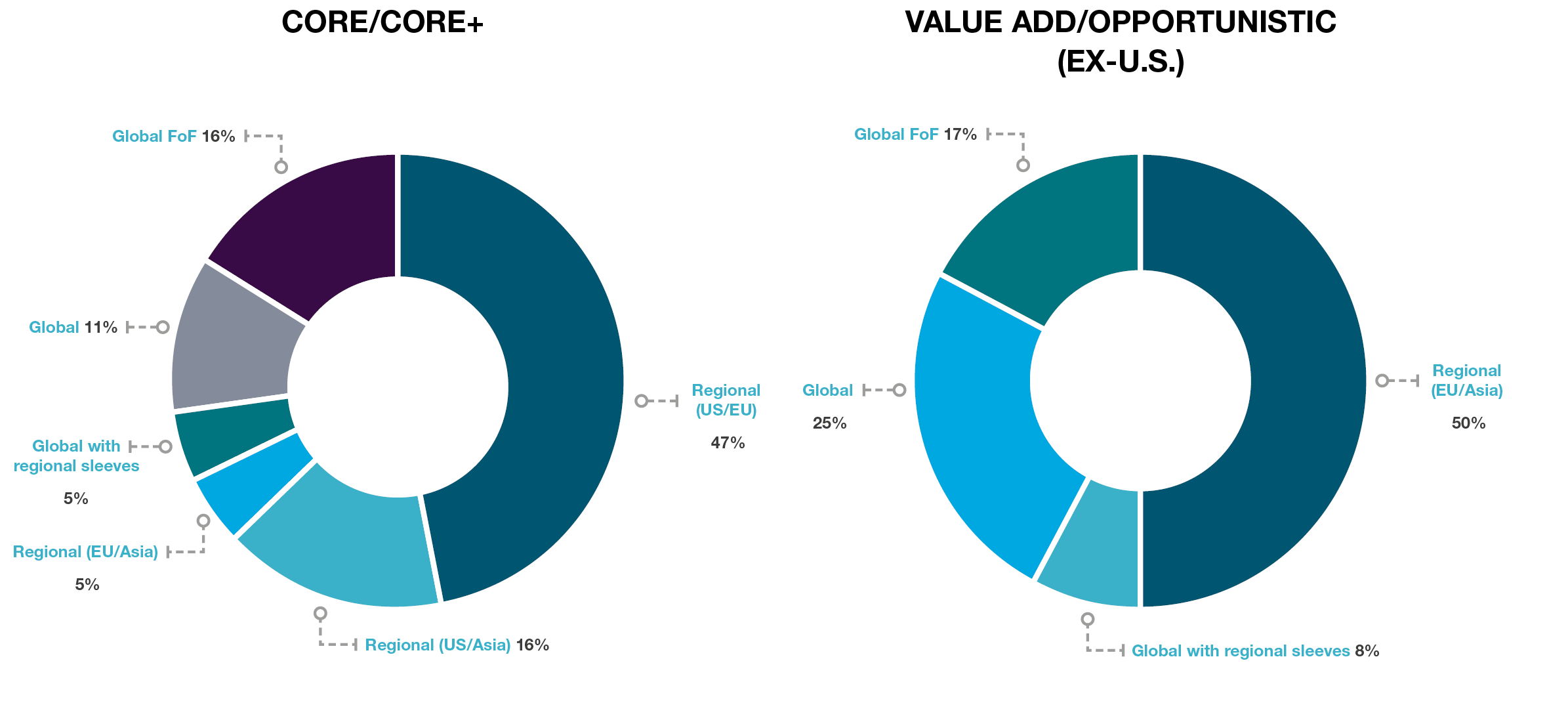

Increasingly investors are exploring these options alongside each other. This is illustrated by two recent searches conducted by bfinance. The first was for a Canadian pension fund looking for global core or core+ strategies and the second was for a U.S. Insurance company seeking global exposure to Opportunistic or Value Add strategies. As the charts below illustrate, true global strategies are still a small minority. Over the coming years, we believe that their number will increase.

Figure 3: Fund options for "global" unlisted real estate exposure

Source: bfinance. Based on number of large cap managers with available funds in relevant regions/strategies from two specific bfinance searches.

As investors consider these options, we need to understand their strengths and weaknesses. One key area of concern is organisational stability. The dramatic growth in the AuM of the largest real estate managers has come not only as a result of organic growth but also through mergers and acquisitions. This is particularly true for managers that have built out global platforms. While consolidation can bring benefits, investors may prefer to avoid mangers that are trying to figure out their organisational structures and cultures.

A FINAL WORD ON LATE-CYCLE INVESTING

Anyone allocating to real estate at this stage in the market cycle should cautiously consider where to deploy their assets, not only in terms of region but in terms of profile: core, core+, value-added or opportunistic.

Although there is a case to be made for all sectors, we find the most compelling opportunities among Core+ and low-risk Value Add strategies with a strong focus on cashflows and modest levels of development, leasing and leverage risk. Opportunistic strategies are potentially exposed to high leverage and development risk in the face of a market downturn; true core strategies are more susceptible to rising yields. Beyond this, investors should seek to understand, in as much detail as possible, how the other risks (development, leverage, liquidity etc) are being controlled by their managers. These distinctions, which can be subtle, will be critical to performance in the years ahead.

Above all, we believe that the priority should be to identify teams and individuals that can be trusted as partners for the long term, through bad times as well as good. While a detailed understanding of track record is important, this should be viewed, alongside culture and alignment, primarily as an indicator of

sustainable partnership.

A condensed version of this article was previously published in PERE News, a global publication focused on private real estate: www.perenews.com.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.