Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

bfinance insight from:

Dr Toby Goodworth

Managing Director, Head of Risk & Diversifying Strategies

Chris Stevens

Director, Diversifying Strategies

This year has been something of a rollercoaster for traditional markets, particularly equities, following a period of sustained low volatility and positive returns. For the year to September 30, Alternative Risk Premia (ARP) strategies have also faced challenges; weaker results primarily stem from poor returns to the Equity Value factor and, to a lesser extent, Trend-Following. Managers are sticking to their knitting, confident in the long-term rationale, while investor appetite remains strong.

After six years of positive average returns for managers within the Alternative Risk Premia space, 2018 is shaping up to be the first year on record when the average ARP manager loses money unless the fourth quarter delivers a strong rebound. We ask: what has happened, and is it likely to dent investor appetite for this rapidly expanding section of the institutional investment landscape?

In order to answer this question, we examine the performance of over 40 ARP strategies, taken from a universe of around 60 providers – a figure which has grown by more than ten since the publication of How Have Alternative Risk Premia Strategies Performed (August 2017) as additional providers have entered the frame.

ALTERNATIVE RISK PREMIA – A BRIEF RECAP

The ARP sector has rapidly expanded in size over the past five years both in terms of assets and number of providers, with investors keen to improve diversification against equity risk and attracted by the prospect of liquid, systematic alternative investments with significantly lower average costs than hedge funds. Demand has come both from investors that have not historically used hedge funds and from those that do but wish to lower costs without materially reducing diversification benefits. Approximately half of the current ARP product universe is readily available in UCITS form.

These strategies seek, on a systematic basis, to provide exposure to various risk premia that have either a well-defined academic/economic basis or a behavioural rationale underpinning a positive expected return over time. Unlike smart beta, that exposure is delivered using non-traditional techniques across multiple liquid asset classes, intended to provide diversification from traditional market risks.

Since this approach is defined by an underlying investment philosophy rather than an explicit strategy, the group is broad and, at the outer edges, hard to define. They vary in terms of performance targets from conservative (cash + 2-3% p.a.) to more aggressive (cash + 8% p.a.), and typical volatility levels range from 4% to 12% p.a. Sharpe ratios commonly sit in the 0.6 – 0.8 range, with a few expecting close to 1.0.

More recently we have also seen the emergence of different flavours of risk premia alongside the “academic” versus “practitioner” groupings outlined in The Changing World of Alternative Beta (2016). Specifically, we now note more “Macro-like” ARP strategies which seek to add additional value through premia-timing in portfolio construction, and more complex ARP strategies that may more closely resemble a quant multi-strategy hedge fund than a classic academically defined ARP strategy.

PERFORMANCE PROBLEMS?

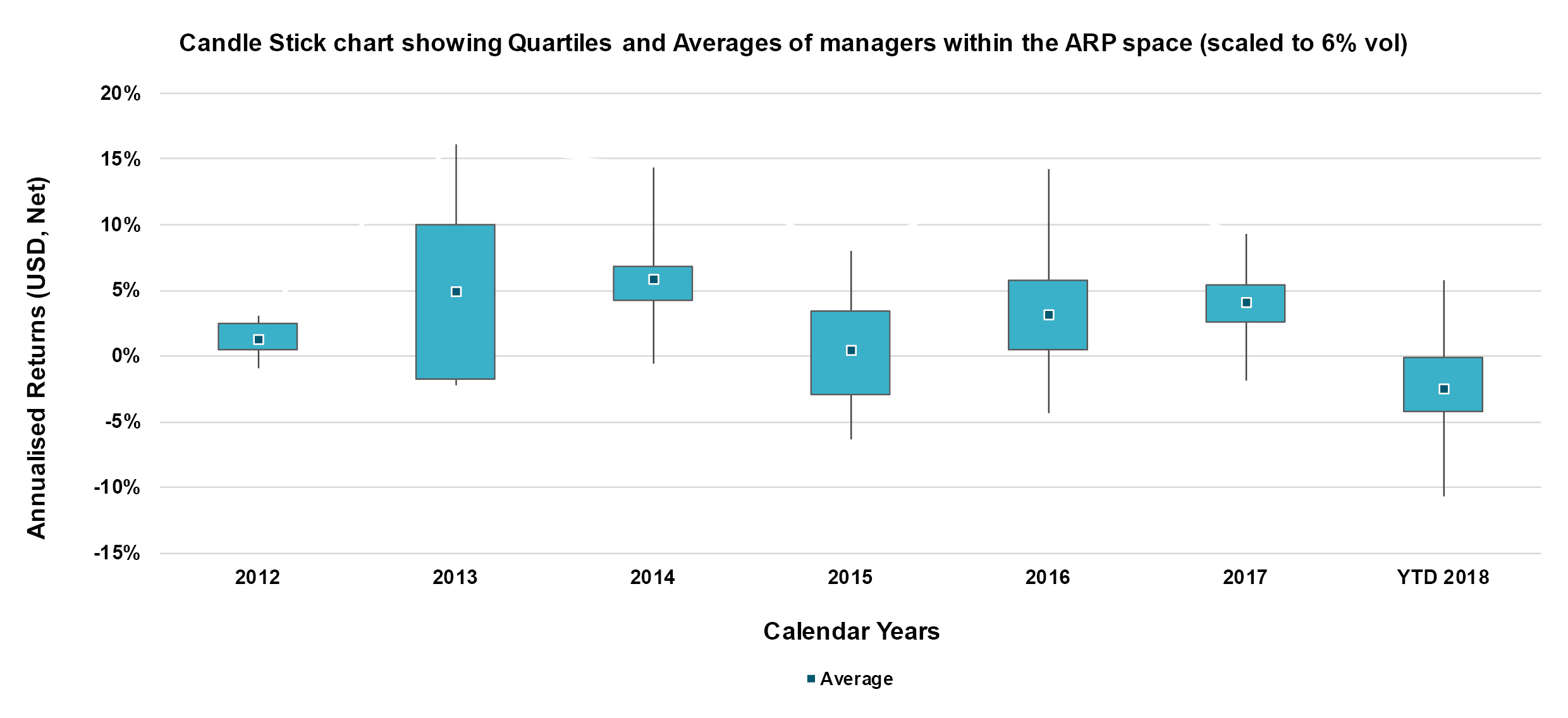

On a cumulative basis YTD (to end Sept), average manager performance in the ARP space sits around -4% net of fees, materially below the median return target of cash + 4–6% and well below the 5.8% average realised net return in 2017. The 3-year annualised performance of the universe at the end of 2017 stood at 3.6%, now down to 2.4% at the end of Sept-2018. This is based on a broad examination of over 40 ARP managers including generalist asset managers, hedge funds and managed futures providers as well as specialist boutiques.

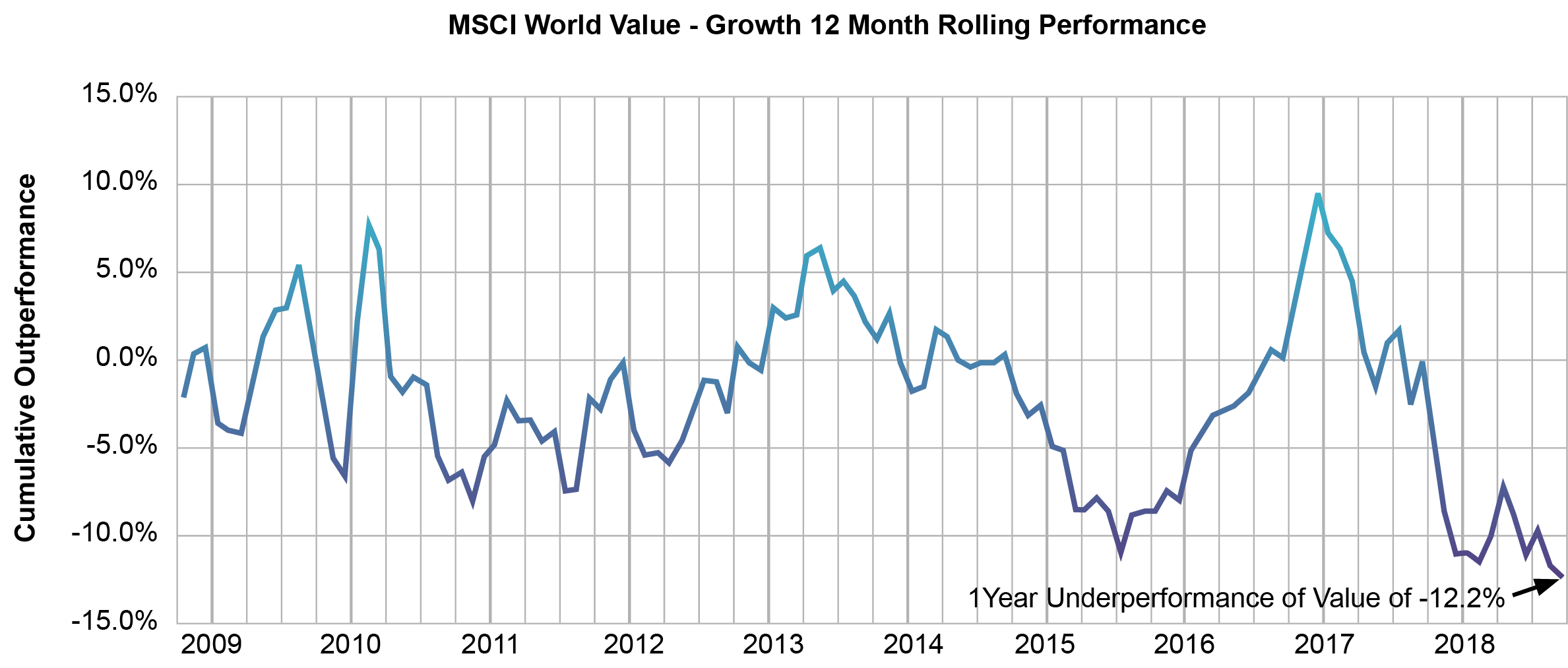

Naturally it is important not to judge any investment strategy on short-term performance: a 3 – 5 year horizon is a more appropriate timeframe. However, it is worth examining the attribution of these 2018 results. In aggregate YTD, Equity Value has clearly been the main source of underperformance with managers across the ARP space reporting losses from their Equity Value strategies regardless of the particular definitions and metrics used to define their approach to the factor. The chart below shows the relative performance of the Value and Growth versions of the MSCI World index; while this would be a very simplistic way of trying to extract the value risk premium, it is instructive in terms of the magnitude and duration of the underperformance of the style. The other notable source of negative return, albeit to a lesser extent, is weakness in trend-following signals.

The drawdown in the Value factor is not unprecedented but is still very significant – the third deepest in last 20 years, ‘beaten’ only by the tech bubble and pre-GFC periods. Several managers have recently produced research to show that previous historic equity value drawdowns have not persisted materially longer than the current one, and have mean-reverted fairly strongly thereafter. While there are no guarantees, we find this to be a reasonable expectation.

Given that Value is a core risk premium for almost all ARP strategies, average portfolio-level losses have – one might conclude – been rather modest. By design, risk premia strategies combine a set of premia return streams that are structurally different from one another, either by asset class or premia type. It is therefore often the case that materially negative performance for a specific risk premium is diluted or mitigated by positive performance from other uncorrelated return streams. This year, cross-sectional momentum and carry-type returns have typically contributed positively to performance, albeit modestly so.

With several different dynamics at play through 2018 YTD, it is useful to dissect the sources of performance by quarter.

Q1 2018: January proved to be a very strong month for trend following, continuing the strong performance seen in Q4 of 2017. Poor performance started in February with a sharp equity reversal (naturally difficult for medium-term trend followers to avoid) along with negative performance (to a lesser extent) from FX and commodities. Simultaneously there was a spike in equity volatility: the VIX was up over 100% in a day, with impact potentially intensified by the previous persistent low volatility environment and the existence of inverse volatility ETFs which were forced to unwind their positions. Not all ARP managers trade short volatility as a premium, but nearly half do and some of these suffered notable losses during this period. Interestingly this was not the case for all managers that traded volatility, with some more active or less directionally driven approaches managing to weather the storm well.

Q2 2018: Equity Value was hit very hard in Q2. This factor seeks to capture the spread premium between undervalued and overvalued assets, with the expectation of mean reversion to fair value. The pain was felt most strongly by those with single stock approaches as well as those that weight equity Value more (typically the more academically focused, and the more market neutral approaches that exclude Trend). In other words, the extent of losses was a product of portfolio construction decisions. Losses tended to be cumulative over the quarter, as opposed to the Trend and Short Volatility losses which were more event-based and therefore sudden.

Q3 2018: Although this was a quieter quarter compared to the first half of the year for ARP strategies overall, the Value factor continued to be weak and Trend saw mixed results. August was particularly strong for Trend, with gains more evident in commodity and FX positions than in equities.

In addition, we see large performance dispersion within the asset manager universe, as illustrated in the first chart above. For those wishing to dig deeper here, the sources of this dispersion are discussed further in How Have Alternative Risk Premia Strategies Performed? (August 2017). For 2018 YTD (to end September), we see this dispersion at near-record high levels, with absolute net returns (normalised to a typical 6% volatility target) ranging from up almost 6% through to down over -10%. Although much of this variation arises from the choice of and weighting to the risk premia themselves, there are also important less obvious contributions from premia definitions and implementation differences, which again underscores the importance of robust manager selection.

It is worth noting that the managers we monitor haven’t exhibited any knee-jerk responses to their investment strategy due to these 2018 results, rather retaining conviction in the economic rationale and empirical evidence underpinning their strategies over the longer term. The period also does not appear to have affected our investor clients involved in this strategy, who have so far maintained their conviction.

TRANSPARENCY IN FOCUS

The last few months have certainly been weak from a performance standpoint. Yet they have been strong from the perspective of clarity. The transparency of these strategies means that poor results can be well explained and understood. Meanwhile, rougher periods can prove instructive for investors who are seeking to scrutinise the differences between managers.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.