Français (France)

Français (France)  Deutsch (DACH)

Deutsch (DACH)  Italiano (Italia)

Italiano (Italia)  Dutch (Nederlands)

Dutch (Nederlands)  English (United States)

English (United States)  English (Canada)

English (Canada)  French (Canada)

French (Canada)

IN THIS PAPER

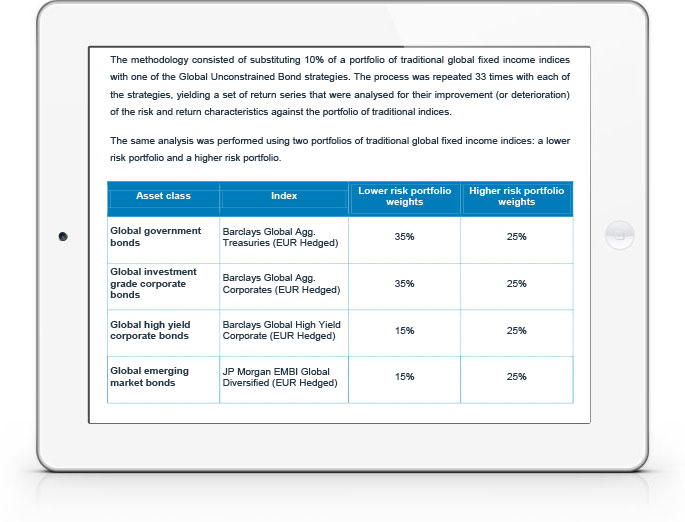

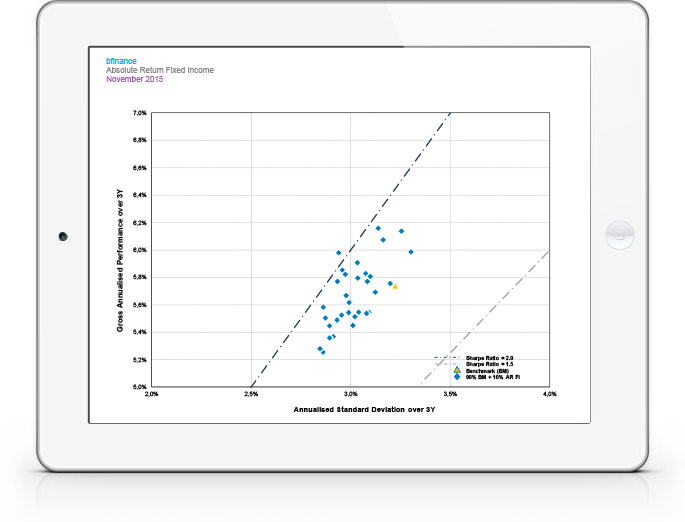

Do absolute return fixed income strategies improve a bond portfolio’s risk/return profile? Portfolio modelling shows the impact of adding a modest absolute return allocation to two different fixed income portfolios. The result: similar returns but a significantly better Sharpe Ratio thanks to lower volatility.

Manager selection brings challenges. These include diversity of objectives, short live track records, capacity constraints, higher fees and question marks over strategy ownership within firms.

What benchmarks and objectives are appropriate? Managers are tending to state a short-term (usually lower) return objective for, and a longer-term (higher) return objective for the full market cycle. We believe that true absolute return strategies with a more ‘market neutral’ approach should be able to achieve their long-term objectives regardless of the low yield climate, especially during periods of heightened volatility. Volatility targets are critical to return objectives.

WHY DOWNLOAD?

The last five years have seen a substantial number of firms launching absolute return fixed income strategies of various types.

There are currently around 100 managers, 60 of which offer a fund vehicle. But strategies with longer track records are rare: we recently identified 40 UCITS funds that had two years of real representative track record at January 2015 and only 16 could present more than five years.

They vary by geographical allocation, sector weighting and beta exposure. Rarely truly global, they often reflect a home bias, with U.S. managers viewing non-U.S. markets as an opportunistic investment. Beta exposure can vary from high (sector-rotation type products with generally higher credit risk) to low (more market neutral products taking long/short trades across rates, currencies and credit markets).

While not all can claim to be truly absolute return oriented or achieve a stable stream of returns, each variation may have its merits. Investors should be clear about the desired function. The primary purpose should be to protect on the downside during turbulent environments and we should not expect high single digit or double digits returns unless strategies are implemented with a level of leverage that is unlikely to suit a UCITS format.

Important Notices

This commentary is for institutional investors classified as Professional Clients as per FCA handbook rules COBS 3.5R. It does not constitute investment research, a financial promotion or a recommendation of any instrument, strategy or provider. The accuracy of information obtained from third parties has not been independently verified. Opinions not guarantees: the findings and opinions expressed herein are the intellectual property of bfinance and are subject to change; they are not intended to convey any guarantees as to the future performance of the investment products, asset classes, or capital markets discussed. The value of investments can go down as well as up.